It’s been a nerve-jangling year for global equities, marked by political upsets and sharp sector rotations.

Even so, the MSCI All Country World Index has defied the odds with a total return of 7 per cent year-to-date, and a number of equity indices are now at all-time highs.

In the region, the MSCI Asia ex-Japan Index has returned a decent 5.3 per cent this year, with the Singapore benchmark lagging behind yet again with 0.5 per cent gain.

And despite some recent setbacks, Asian bonds as measured by the JP Morgan Asia Credit Index rose 5.8 per cent over this same period.

So have investors who remained on the sidelines missed the boat? We don’t think so.

NOT ALL IS DOOM AND GLOOM

2017 will likely shape up to be a good year not just for United States equities, but also emerging markets.

True, US President-elect Donald Trump’s unexpected election victory has raised fears over capital market disruption, while the extent of his protectionist policies remains a source of vulnerability for the region.

But not all emerging markets are made equal.

Latin America sends 47 per cent of all its exports to the US.

Asia, by contrast, trades with a more diverse group of nations, and ships just 16 per cent of all its exports to the US.

Among emerging economies with large domestic markets, particularly Brazil, China and India, we see opportunities for outperformance.

What’s more, while the repricing of inflation expectations in the US should continue – we like inflation-protected bonds in the US – further rises in US yields are likely to be gradual.

Read Also: What a Trump win means for Singapore

With the size and timing of potential fiscal stimulus still unknown, the Fed’s moves will likely remain gradual to help heal the labour market.

Secular forces – ageing demographics, the preponderance of savings over investments and low productivity – should also work to keep longer-term interest rates anchored.

We expect the 10-year US Treasury yield to be no higher than 2.3 to 2.5 per cent by end-2017, likely blunting the current momentum seen in the US dollar.

While Mr Trump’s election is a potential setback for globalisation, the pro-growth elements of his proposals – tax cuts, fiscal spending and deregulation – are reflationary.

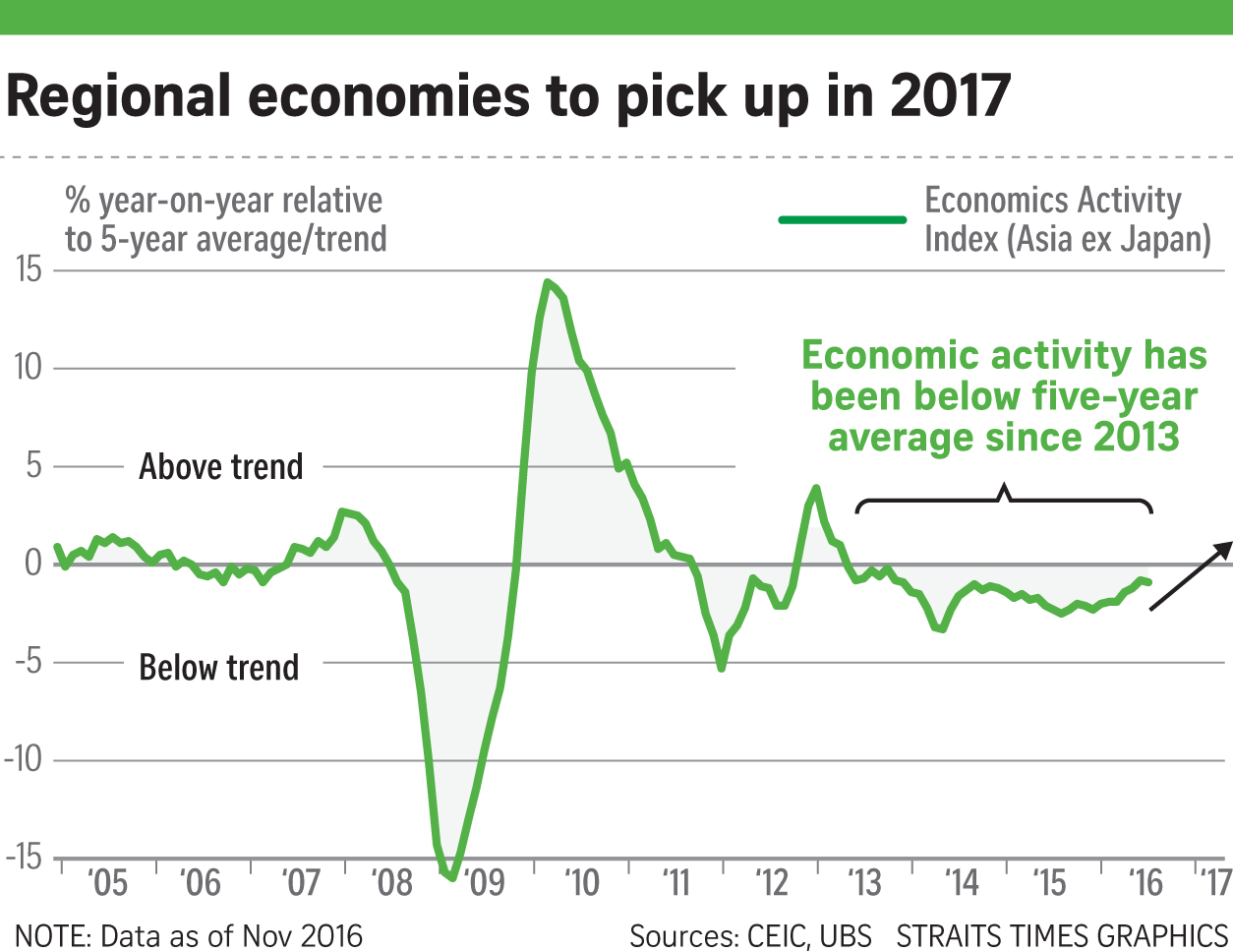

Historically, this has led to positive spillovers on Asia, which remains on track for a year of stronger nominal GDP growth, high single-digit earnings recovery and gradually higher lending rates.

Aside from US politics, Asia has its own reform dynamics to contend with in coming years.

The current batch of determined leaders in Asia, many backed by strong popular mandates, lifts the chances of success as the region ploughs ahead with technology and infrastructure upgrades, and industrial renewal.

For China, ahead of the critical political leadership transition in late 2017, Beijing will likely emphasise reasonable growth and financial markets stability, with critical reforms in state-owned enterprises and overcapacity sectors staying gradual over the next 12 months.

ASIAN EQUITIES SHOULD OUTPERFORM BONDS IN 2017

We remain positive on Asian risk assets with a preference for equities over investment grade bonds.

As producer prices rebound and return-on-equity recovers, we expect Asian equities to deliver low-teen returns next year, with an overweight on China and India, versus an underweight on Taiwan and the Philippines.

Singapore is a relative beneficiary of a steepening yield curve and valuations near decade lows should offer downside support.

But while valuations are inexpensive, we expect the market to trade range-bound in the absence of growth catalysts.

With historically low yields still on the horizon, the search for yield may prevail.

But with higher inflation and likely three Fed hikes from now till end-2017, private investors need to be more selective.

“Yield with growth” stocks typically found in Asian cyclical sectors, including consumer discretionary, materials and IT, should outperform.

As bond proxies, Reits would likely be impacted by the ongoing rotation out of defensive equities.

Still, selected Reits from Australia, Singapore and Hong Kong with cyclical growth potential, acquisitive opportunities and conservative debt-hedging profiles should remain well-supported in a gradually higher yield environment.

Within Singapore, we prefer ungeared yield (that is, dividends paid out of a net cash position) over leveraged yield amid rising interest rates.

A sustained increase in interest rates bodes well for banks.

Thematically, “growth at a reasonable price” strategy remains rewarding and we like the new economy and technology leaders.

Read Also: Chinese business execs not worried about Trump getting tough on them

Asian financials and blue-chip cyclicals in the consumer discretionary and materials industries also offer attractive value.

The recently announced Shenzhen-Hong Kong Stock Connect will be a catalyst for the China market and Hong Kong-listed small- and mid-cap stocks.

However, we are less excited about Asian credits, given their stretched valuations, weakening credit quality and increasing supply.

Still, Asian bonds are likely to be more resilient than their global counterparts, due to the higher credit quality of issuers and support of local investors.

In the year ahead, we expect most Asian currencies to gain some ground against the US dollar as the Fed tightens policy gradually and the US twin deficits receive greater attention.

Within the region, higher inflation and a better growth backdrop should spur Asian central banks to shift to a more neutral stance.

Of course, US protectionism is the major unknown.

We enter 2017 preferring high-yielding Asian currencies like the Indonesian rupiah and the Indian rupee.

Conversely, we expect the Singapore dollar and the Chinese yuan to underperform.

Investing in Asia this year was not for the faint-hearted. Next year will likely be no different, given increased policy uncertainty in the US and political risks in Europe.

Still, the underlying economic and earnings fundamentals matter more.

Investors should take a well-diversified investment approach, and be more nimble in 2017 than in recent years.

This article was first published on December 5, 2016.

Get a copy of The Straits Times or go to straitstimes.com for more stories.

{kind=link}